May 4, 2026 · Market Report

Two Economies. One Market. Why Seattle Real Estate Won’t Cooperate With the Headlines.

As of this week, 92,000 tech workers have been laid off in 2026. That works out to 864 people a day, every day since January 1st. Last week alone, Meta cut 8,000 jobs and Microsoft offered buyouts to another 8,750 employees. The same week, Amazon committed an additional $25 billion to Anthropic. Meta broke ground on a $1 billion AI data center in Oklahoma. Microsoft’s AI infrastructure budget for calendar year 2026: $190 billion.

The companies doing the most cutting are also doing the most spending — just on compute instead of people. This isn’t a tech downturn. It’s a conversion. And understanding that distinction is the most useful thing I can offer anyone trying to make sense of Seattle’s real estate market right now.

The Iran Variable Nobody Budgeted For

The spring market was building toward something. By late February, the 30-year fixed rate had dropped below 6% for the first time in four years — real buyer momentum was returning. Then the U.S.-Iran conflict broke out, the Strait of Hormuz was effectively shut down, and the International Energy Agency described it as the largest oil supply disruption in the history of the global energy market. Within days, mortgage rates were back above 6.1%. By early April they’d climbed to around 6.45%. Existing home sales slid to a nine-month national low.

Gas hit $5.72 a gallon in Washington. Higher oil feeds higher inflation expectations. Higher inflation expectations keep the Fed parked. The Fed parked means rates don’t move. That’s the chain, and it’s why the rate environment buyers are navigating right now is more complicated than it was four months ago — not because of anything that happened in Seattle, but because of what happened in the Persian Gulf in late February.

Two Economies, One City

Economists have started calling it the E-shaped economy — three tiers of consumer behavior running in parallel. At the top, households earning $125,000 or more have seen 7.6% real spending growth since 2023. Middle earners, around 3%. Lower earners, just over 1%. The top 20% of income earners now account for 60% of all personal spending in the country. McDonald’s has been adding value deals trying to win back customers who stopped showing up. Premium restaurants are full.

Seattle is not a McDonald’s economy. King County’s median household income sits well above the national average, and the concentration of six-figure tech, biotech, and professional services employment here is among the highest of any metro in the country. The layoffs are real — approximately 16,590 Seattle-area tech workers were affected in Q1 2026 alone, and more cuts landed last week with Meta and Microsoft. But the roles being cut are concentrated in corporate support, HR, recruiting, operations, and middle management layers. The senior engineers, AI specialists, and infrastructure workers that drive demand for homes in the $1.2M to $2.5M range in Ballard, Capitol Hill, Queen Anne, and Madison Park were largely not in those cuts. And many of those who were displaced are landing back in the region within a few months, because the region keeps pulling them back.

Here’s the counterweight that isn’t in most of the layoff headlines: four companies are in active discussions with Seattle City Light about building five large-scale AI data centers inside the city limits. Combined potential demand of 369 megawatts — roughly a third of what Seattle uses on an average day. That’s construction employment, infrastructure investment, and a sustained pipeline of high-earning technical workers who will need housing. Seattle is increasingly described by analysts as the second capital of American AI, behind only Silicon Valley. The layoffs and the buildout are not in opposition. They are the same story told from two sides of the same balance sheet. Companies are converting human capital into compute capital, and the conversion is happening inside Seattle’s borders.

The Real Estate Industry’s Own Consolidation

The brokerage world has been doing its own version of this restructuring. Compass — the platform Madeline and I work through — closed its acquisition of Anywhere Real Estate on January 9th. Coldwell Banker, Century 21, Sotheby’s International Realty, ERA, and Corcoran, all under one roof now. The combined platform runs roughly 340,000 agents globally with an enterprise value around $10 billion. Then last week, The Real Brokerage announced it’s acquiring RE/MAX Holdings for approximately $880 million — 145,000 agents, 8,500 offices, operations in more than 120 countries, folding into a new entity called Real REMAX Group. That deal closes sometime in the second half of 2026.

Two of the largest brokerage transactions in the history of American real estate, months apart, both bets on the same thesis: scale and technology are where this industry is heading.

What it means for anyone buying or selling in Seattle is less dramatic in the short term than the announcement suggests. The transaction itself — the financial, emotional, legal complexity of moving the place where your life happens — still comes down to the individual agent you’re working with. A deal structure in Miami doesn’t change what it feels like to negotiate through a difficult inspection period on a Queen Anne Victorian. What changes over time is the infrastructure behind those agents — data access, pricing precision, off-market inventory. I’ll acknowledge the obvious bias: Compass is our platform. But I think consolidation around technology-forward brokerages is genuinely good for clients who know how to use it.

What the Market Is Actually Doing

With rates sitting at approximately 6.39% — the Federal Reserve held steady at its last meeting, with inflation still above target and no rate cut timeline in sight — the active buyer pool is smaller than it was at peak frenzy. But it is serious. The people transacting right now have done the math, accepted the rate environment, and made their decision. That tends to produce cleaner deals than the speculative fever of 2022.

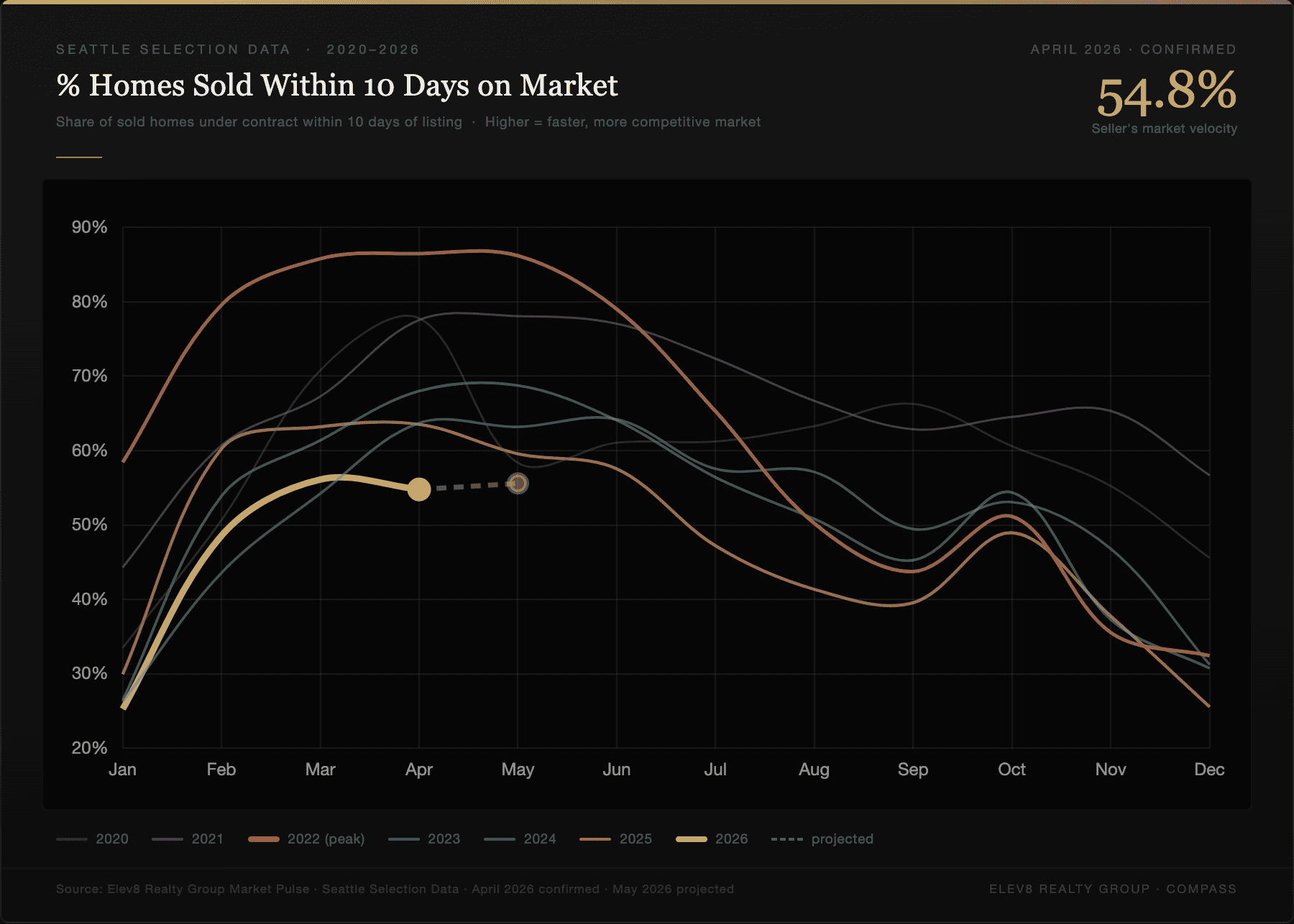

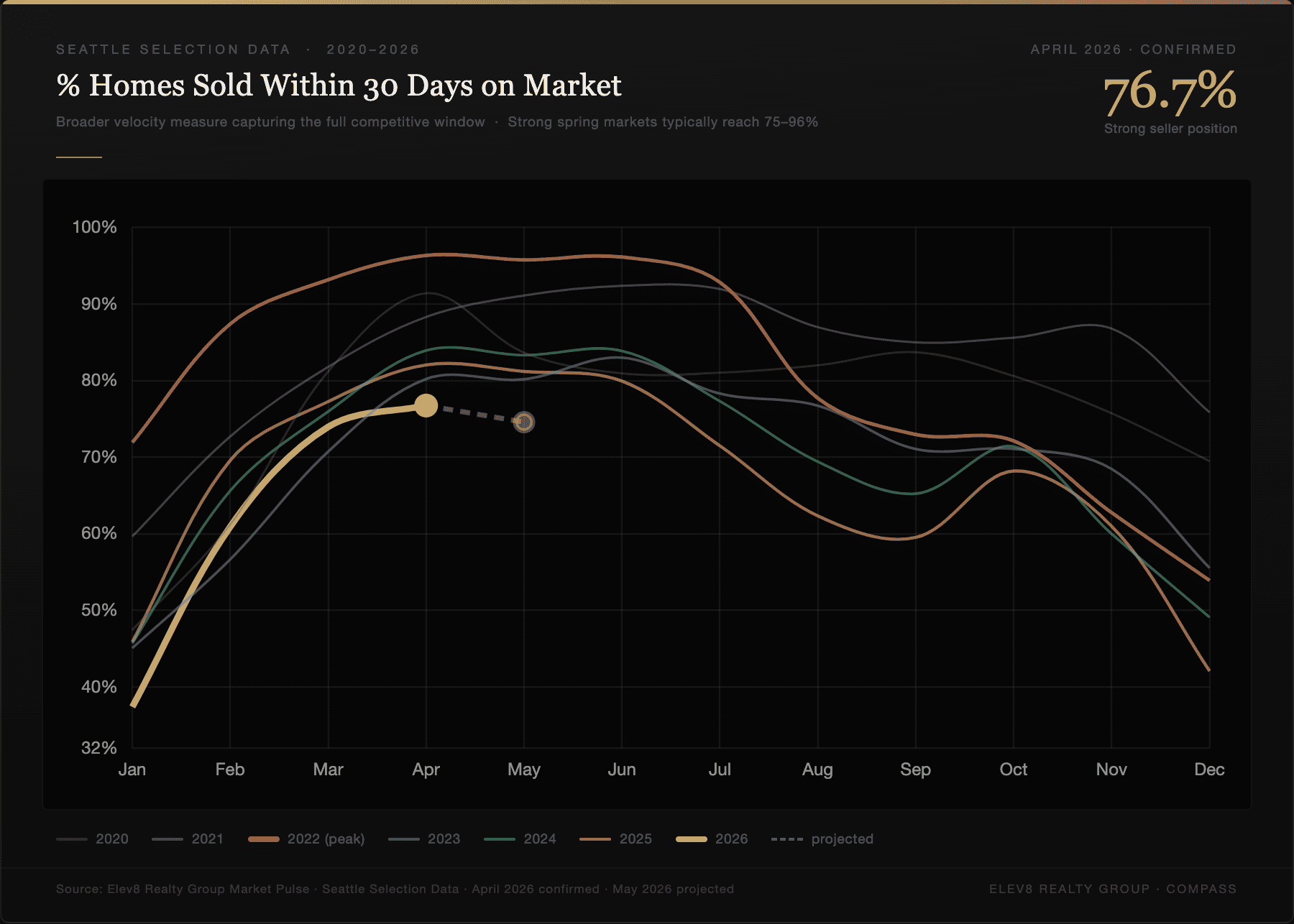

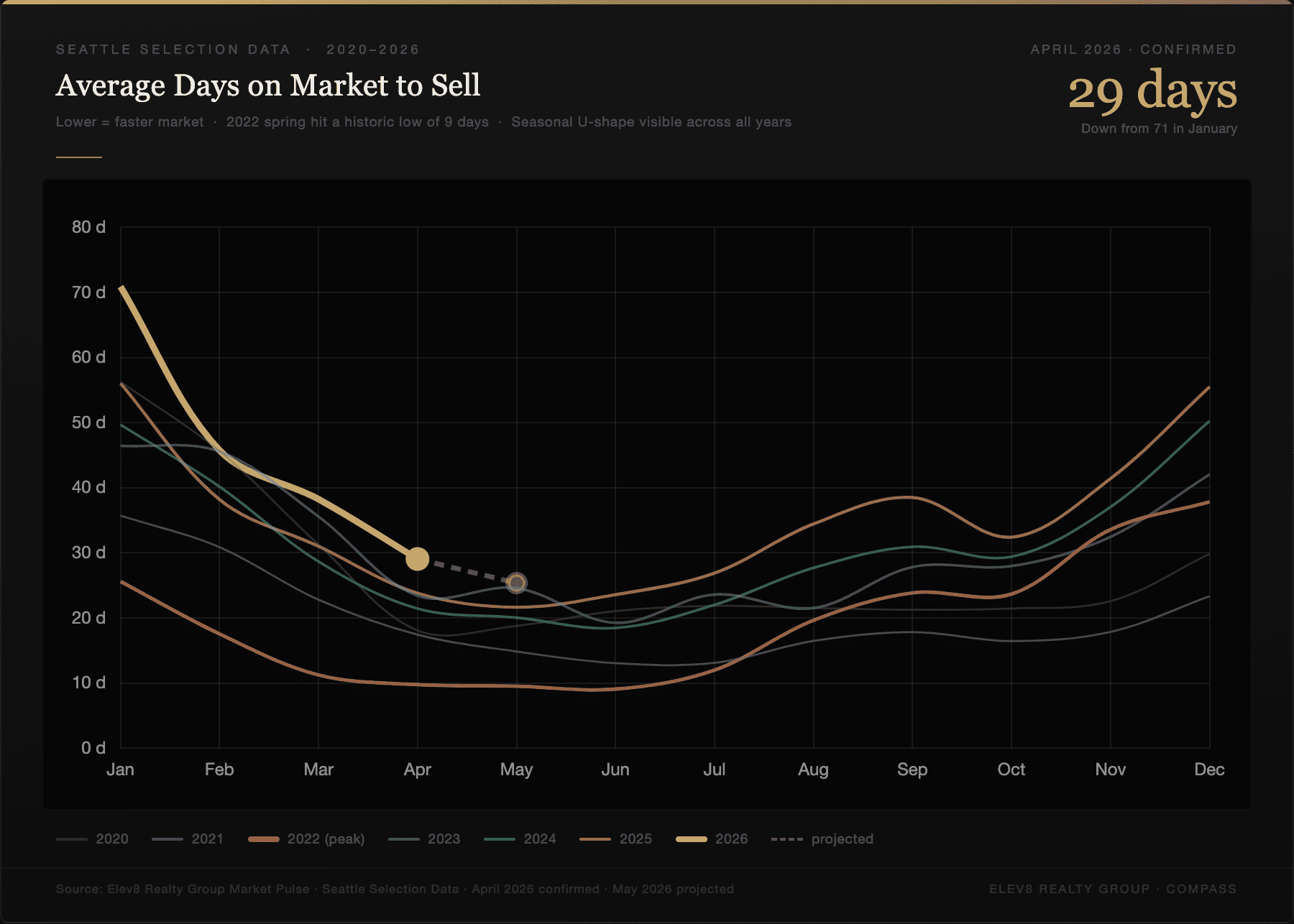

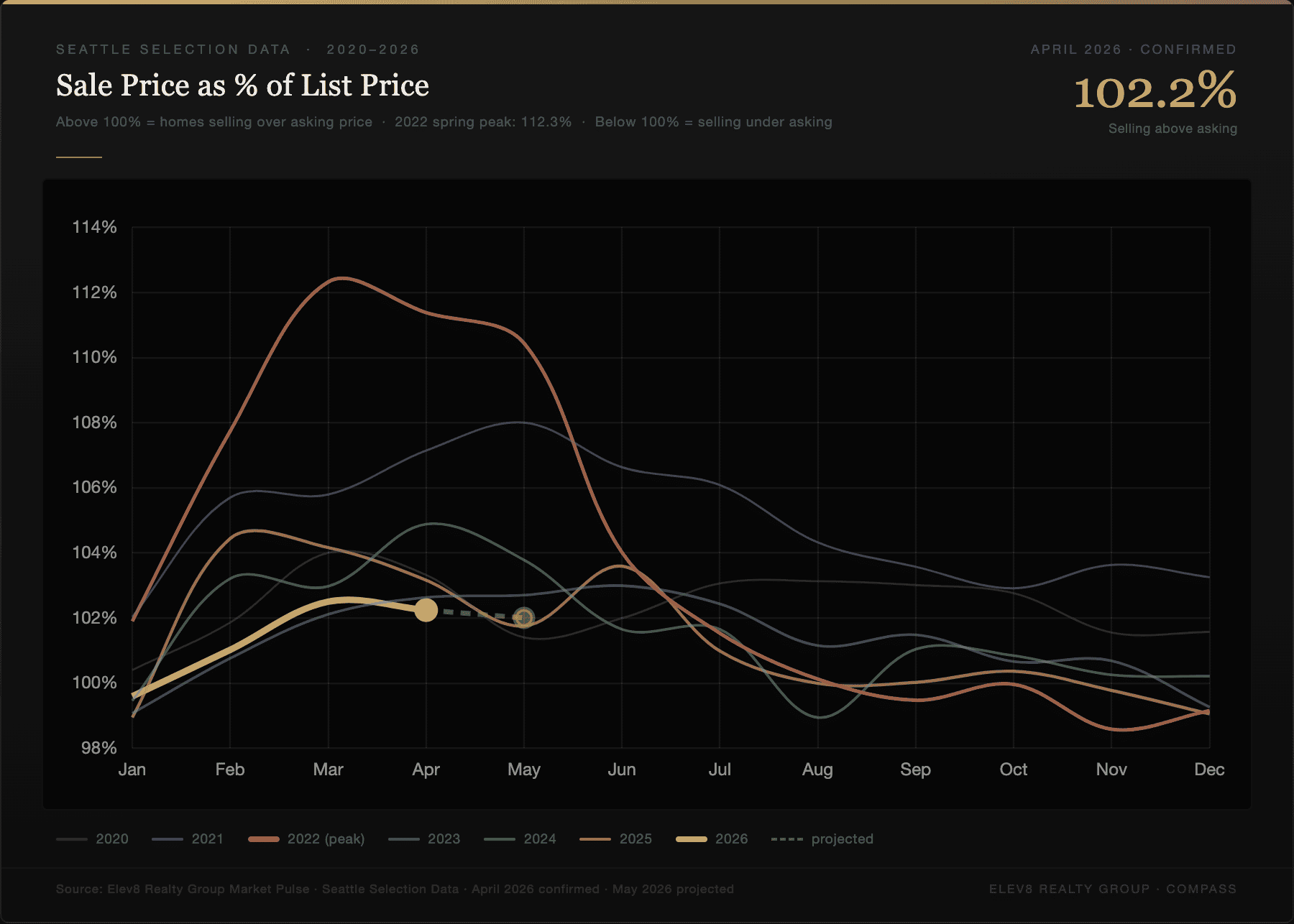

Our internal Market Pulse tracking, which monitors pending activity across a consistent Seattle selection throughout the season, confirms the spring market is genuinely competitive. More than half of homes are going under contract within the first 10 days. Homes are still, on average, closing above their asking price. Days on market are sitting around 29 — slightly longer than in recent years, but meaningfully tighter in recent months with leading pending data showing a continued improvement into May at approximately 25 days on market to sell.

For context: in April 2022 at peak froth, 86% of homes sold in the first 10 days, and the average sale-to-list ratio was 111%. We are not in that market. We are also not in a buyer’s market. We’re in a seller’s market that has rediscovered its judgment — and that, in my experience, is where the most durable transactions happen.

54.8%

Sold in first

10 days on market

76.7%

Sold within

30 days on market

29 days

Avg. days on

market to sell

102.2%

Sale-to-list ratio

homes selling above asking

Five Charts · The Spring 2026 Picture

Each chart below traces the same Seattle Selection Data across seven years. The bright gold line is 2026 confirmed through April; the dashed extension is the projected May reading from leading pending activity. Historical years are shown for context.

What This Means Practically

On the selling side: Sellers who priced for today — not for the comparable sale from 18 months ago — are moving fast and moving well. The listings I’m watching sit are not sitting because of the economy. They’re sitting because the opening price didn’t match the market’s current temperature. That gap is closing on its own, just slowly and painfully. The sellers who get ahead of it are capturing better outcomes than the ones who need three price reductions to find their buyers.

On the buying side: The formula right now is straightforward, even if it’s not easy. Full underwriting, not just pre-approval. A clear scope — knowing which neighborhoods and which trade-offs you can live with. And the ability to move within 24 to 48 hours when the right property surfaces. That combination is beating higher offers that aren’t as clean. I have watched it happen this spring repeatedly.

The macro backdrop — global tensions and an active war in the Middle East, tariff uncertainty, Fed ambiguity, brokerage dealmaking — will continue for the foreseeable future. But none of it touches the structural supply problem that has defined Seattle’s housing market for a decade. That doesn’t reverse because the headlines get louder. The people who understand the difference between the national story and the local one tend to make cleaner decisions than the people waiting for a moment of clarity that probably isn’t coming in the form they’re expecting.

The spring window is real. Summer typically softens the competition. If you’re trying to work out what the timing means for your situation specifically, reach out.

— Anton

Anton K. Alexander is a Broker with Elev8 Realty Group at Compass.

17+ years in Seattle real estate. $700M+ in career sales representation.